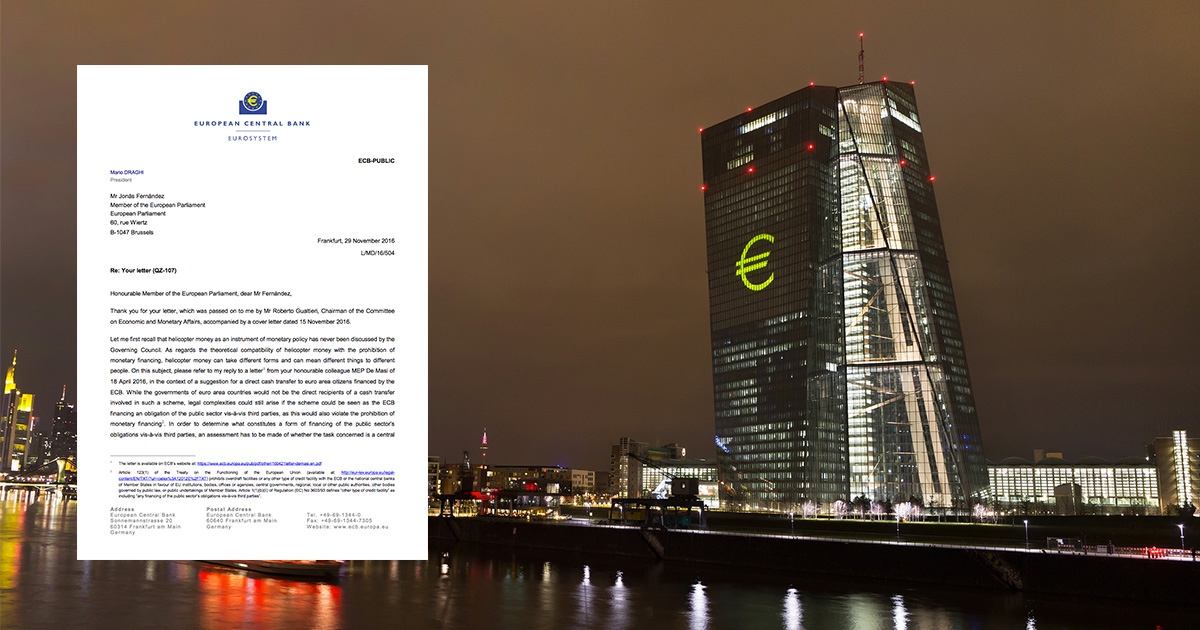

Instead of injecting the equivalent of €2.2 trillion into financial markets, the ECB could have injected a quarter as much money and distributed €1,000 to all adult citizens in the eurozone.

The European Conservatives and Reformists (ECR) group in the European Parliament recently launched “Leer Geld”, an initiative led by MEP Sander Loones, to raise awareness about the effects of the monetary policy conducted by the European Central Bank (ECB).

The initiative is to be welcomed: monetary policy is too often overlooked by civil society, yet its impact on our lives has never been greater. Under its “quantitative easing” programme (QE), the ECB has been buying large quantities of government bonds since 2015. Surely injecting the equivalent of 20 percent of GDP into the eurozone finance sector cannot be without consequences. Continue reading “ECB should design, decide and implement the helicopter money programme”